Each new season in the tech world passes under a new term, as if under the zodiac sign. 2017 was marked by ICO, 2018 – by blockchain. 2021 seemed to be the year of NFT, but NFT was later replaced with Meta. From Meta the tech world jumped to even vaguer and undefined term – Web3.

We have been moving to the Web3 era for the past six months. Are all market players really ready for this?

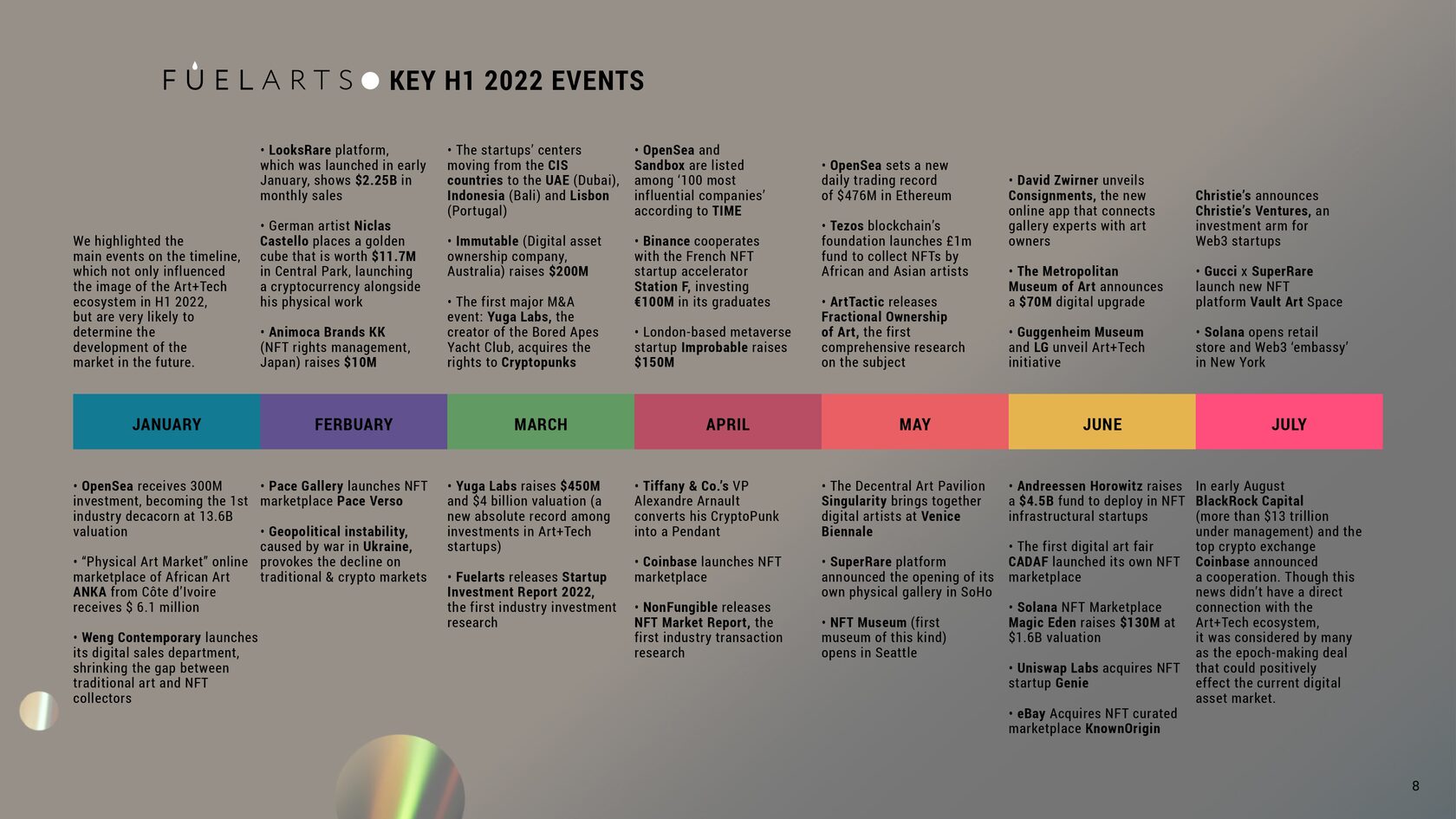

H1 2022 started with the appearance of the first Decacorn – OpenSea at the Art+Tech market in January (valued $13.6 billion), and ended with the BlackRock Capital and Coinbase collaboration early in August. What could we see in between?

The crypto-winter, which many people have been frightening with since the autumn of 2021, has finally been confirmed. True, a sharp decline in the digital economy had to be aggravated by additional factors - the war in Ukraine and inflation in a number of the world's largest economies. We rejoiced last year at the news when another traditional investor made a serious purchase of bitcoin. We saw the outcome in March, 2022: investors sold both hard assets and crypto savings in an effort to bail out the cash flow. In other words, the correlation between the fiat and crypto markets has become very high. And now neither bitcoin nor NFT can save us from the crisis, while previously it was the other way around.

However, this situation did not scare off investors of pre-planned rounds, who, following the OpenSea, went on disturbing media with high amounts of investments. Thus, the first 6 months of 2022 saw 8 rounds of Art+Tech & NFT startups exceeding $100 million. The record one-time deal also fell on that period: Yuga Labs (Bored Ape Yacht Club) received US$450 million in March, i.e. 3 times more than Artsy since its foundation.

Another thing is that NFT sales volumes have significantly decreased at the same time, as the main news-making asset of today's market. It decreased from $10.7 in Q1 to $8.1 in Q2 2022 (-24.8%) in monetary terms according to NonFungible. Nevertheless, investment continued to flow into the sector.

To understand the secret, we offer to look at the events of H1 2022 from the perspective of an ordinary investor encountering the Art+Tech & NFT market for the first time. These are not sales volumes at marketplaces that matter for him or her, while stepping into a new territory, but completely different factors. Namely, 4 features of a healthy ecosystem:

• Infrastructure

• Reports

• Academic research

• Attention of strategists

Infrastructure. We see an ecosystem of 801 startups with public investment data, and several hundred more in the Bootstrap phase. All links of the Value Chain - R&D (creation), Trade, Management, and Analytics - are filled with young companies operating at the market. There are also at least 33 specialized investment funds having raised more than $23.7 billion for startups that have moved to Web3.

Reports. Today, there are 7 specialized reports on the Art+Tech & NFT market (5 of which appeared in H1 2022). They cover all aspects of the market - from asset sales and the development of blockchains and metaverses to investments in infrastructure. In addition, at least 5 "traditional" art market reports have begun to include technology-related sections in their releases. In other words, the investor has something to focus on in terms of market movement.

Academic research. There are more than 20 institutional (at the level of academic papers or full-fledged Ph.D.) works exploring the Art+Tech & NFT market in 2022, e.g. the analysis of the behavior of the audience of buyers of digital assets, or the principles of building a career for NFT artists. Students’ term papers at Sotheby's Institute of Art and Christie's Education, etc. are on their way.

Attention of strategists. We may have the greatest diversity here, even against the general optimistic background. Top players in the commercial sector, such as Kering (Balenciaga, Gucci etc.), LVMH (Tiffany, TAG Heuer etc.), Nike, have joined the NFT operations. Attention to Art+Tech startups as investment objects was payed in 2022 by Microsoft Ventures and Samsung Ventures. The largest startup strategist Animoca Brands has announced the establishment of an ecosystem of 340 Web3 subsidiary startups. Such strategic ecosystems are currently established by the largest blockchains (Solana, Polygon etc.) and crypto exchanges (Binance, Uniswap etc.). Finally, the giant of the traditional art market, Christie’s auction house, announced the establishment of a venture arm in July, 2022 to fund Art+Tech startups.

In other words, new Art+Tech & NFT infrastructure investors see all the signs of a healthy emerging market. And the next question for them is how ready they are to participate in it, given their own priorities in the current economic situation.

We also consider it necessary to return to the main problem outlined by the participants of the previous Fuelarts survey (January, 2022). Namely, the link between the physical and digital markets at the level of collectors and artists from different (so far) parties. A certain work was carried out in this regard in H1 2022: the physical spaces of the SuperRare marketplace and the Solana blockchain in New York were made operational against the backdrop of the slow work of auction houses with NFT. And, let the sales of branded sneakers and hoodies so far go better than those of pieces of art presented on the displays - but the first step into the physical world has already been taken.

Similarly, the attitude of traditional collectors towards digital art is gradually changing. According to HISCOX Online Art Trade Report, conducted by ArtTactic (April, 2022), 41% of the NFT art buyers prefer curated marketplaces – compared to 27% of adherents interested in the 'flea market' of NFT platforms. At the same time, 84% of traditional collectors said the digital shift in the Art Market would become permanent, up from 51% in 2020. As a quick snapshot, for the first 4 days of May, the total trading volume on the TOP-8 curated NFT marketplaces was exactly the same as for all 30 days of April ($102 million).

In other words, we see the growing recognition of the artistic value of digital art. This is not a quick process, which will be accompanied by a drop in NFT sales on the ‘flea market’ platforms – but these were the steps also taken by the traditional art market. Though the division into highly artistic and decorative art took place as early as the 16th century ... but we are ready to wait, aren’t we?

And now it is high time to return to Web3. Don't you think that this term seems to have been born in order to reconcile both sides of the same market, as an umbrella covering both physical and digital collectors? There will be no strife created by provocative questions - say, what kind of art are you an adept of? After all, there will be the only answer: “We are the Web3 era collectors.”

We are through with investors and collectors. And what about startups?

Startups put Web3 to their presentations in 2022, without even knowing what stands behind Web1–Web3 revolution. The desire to create an image of a progressive company leads them to a dead end, while simple questions from investors reveal their lack of knowledge. In media, Art+Tech has been also replaced by Web3 term, which unfortunately does not make the market more transparent for new investments.

Whatever happens, Art+Tech remains Art+Tech. However, we believe it will be divided in a short time into Web2 Art+Tech and Web3 Art+Tech depending on the level of technology that young startups will profess. This division will provoke founders to switch to the latest technologies, giving them higher chances in fund raising activities.